May 2026

The Realtor.com published a 2026 Housing Market Forecast that provides insight into expectations of what will happen on a national level:

Home Sales To Remain in Low Gear as Balance Holds. 2026, we expect a steadier housing market, but it’s not yet off to the races. Mortgage rates are forecast to average 6.3%, easing affordability pressures slightly, while home prices rise modestly by 2.2%. Existing-home sales should climb about 1.7% to 4.13 million, a small but meaningful gain from 2025’s near 30-year low. At the same time, for-sale inventory will continue to recover, up nearly 9% year over year.

For homebuyers and sellers, the shift signals a more balanced market—one where price growth steadies, rate relief offers breathing room, and negotiating power tilts subtly toward buyers. Housing affordability improves as incomes outpace inflation, pushing the typical payment share of income below 30% for the first time since 2022. Meanwhile, renters benefit from softening rents—especially in the South and West.

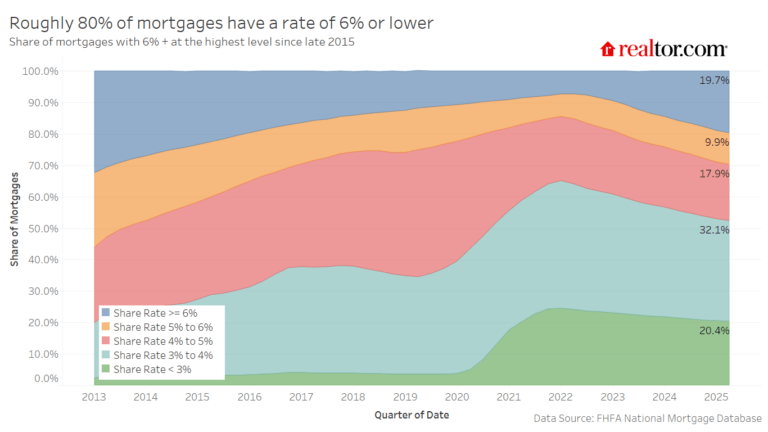

The mortgage rate lock-in effect—caused by market rates that are well above the rates on existing mortgages—has left many homeowners with a strong reason to stay put. In fact, recent data showed that 4 out of every 5 homeowners with a mortgage has a rate below 6%. The share has waned gradually, a trend that will continue in 2026. As a result, turnover will be limited with moves likely to be spurred by life necessities such as job or family changes.

We project an 8.9% increase in active listings in 2026, marking a third consecutive year of gains. The pace of improvement has slowed, however, as the market edges closer to pre-pandemic norms. By year’s end, nationwide inventory levels are expected to remain roughly 12% below pre-2020 averages, an improvement from a 19% gap in 2025 and nearly 30% in 2024.

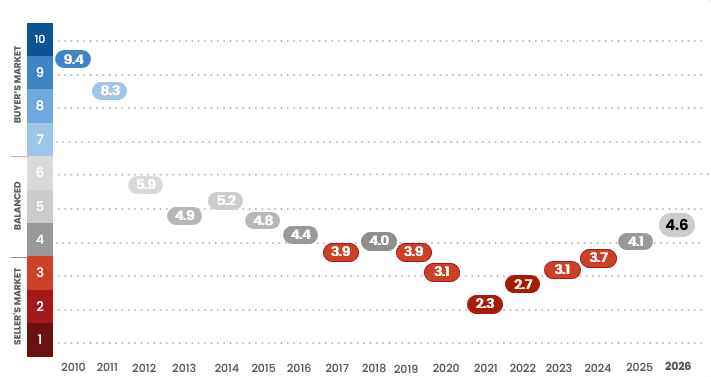

The national housing market will remain in balanced territory in 2026, averaging 4.6 months of supply across the year. Even so, momentum in the housing market is expected to tilt toward buyers as a more substantial growth in the number of homes for sale than homes sold shifts the balance of supply and demand. Housing affordability will remain a stumbling block for many, especially younger and first-time buyers, but negotiating power is expected to improve.