July 2026

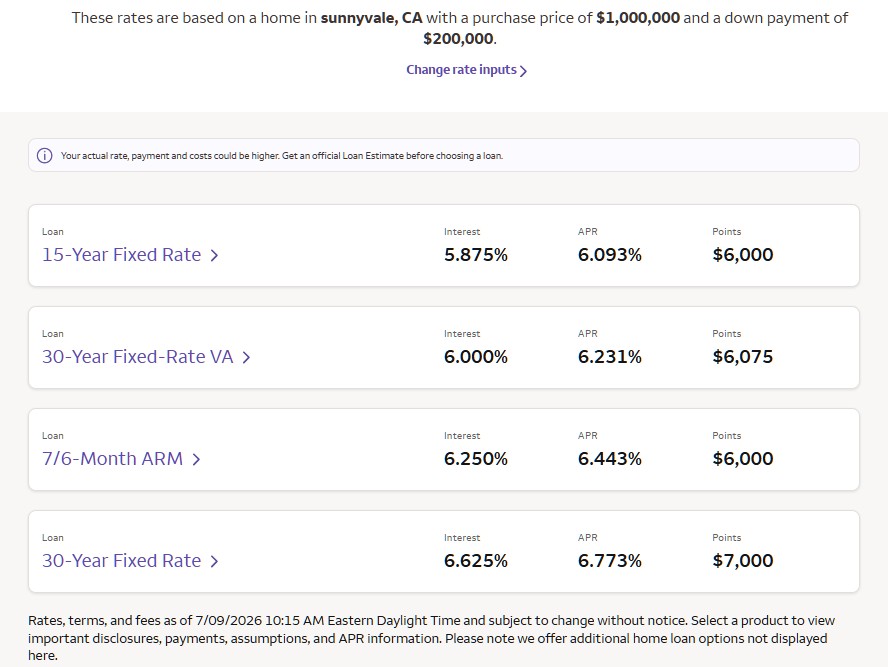

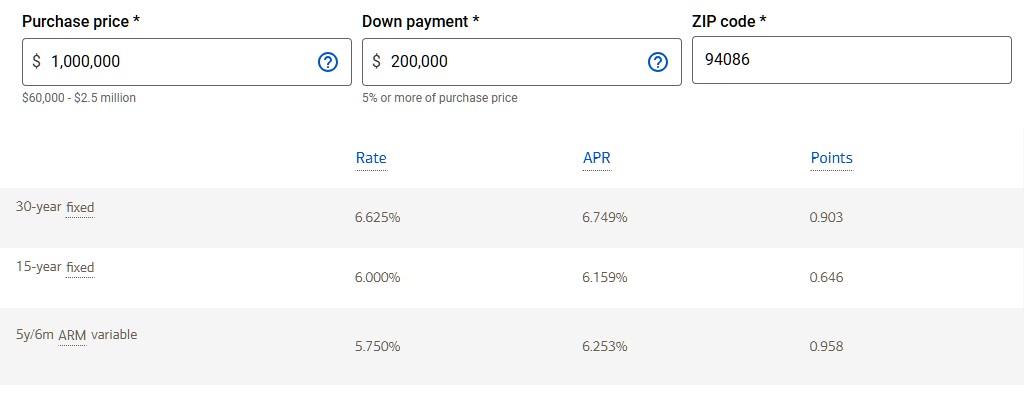

Interest rates vary fairly significantly. The biggest factors being whether the loan amount is conforming or jumbo and if the size of the down payment. Understanding what the rate is for your situation is critical in determining your target purchase price. Below are examples to help understand the financing market. I highly recommend talking to a lender to have them explain your options and run the numbers.

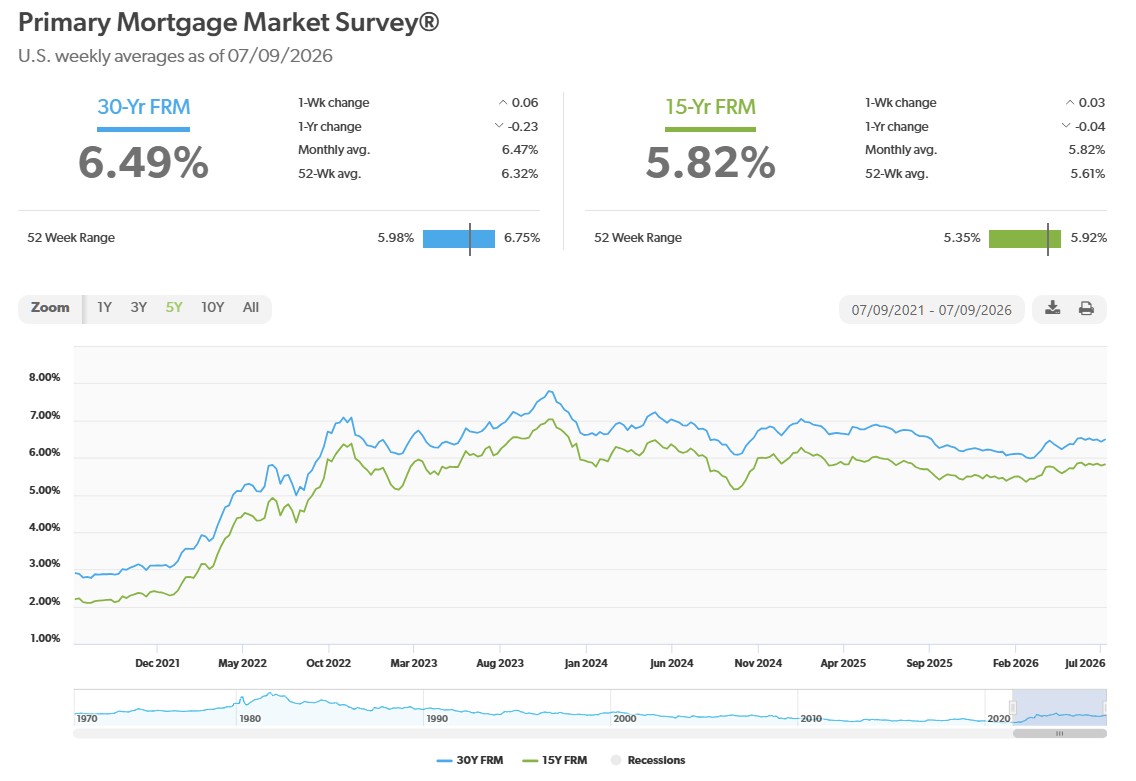

The financial news usually uses the Feddie Mac PMMS Mortgage Market Survey that shows the national weekly average.

Rates also vary depending on your credit score. Wells Fargo considers 760+ as excellent and 700-759 as good. Not clear what credit score the above rates are based on. I suspect a good score with an excellent score reducing the rate by 0.175 to 0.25 points.

Talking to one of the lender’s mortgage advisors is a great way and a no-charge way to make a first pass at this. I recommend clients to check with their existing bank to have them explain the different loan programs and their rates. More importantly, they can run the numbers to determine how much of a loan you would qualify for.

My final recommendation is to not let high interest rates discourage you from investigating a home purchase. Most buyers can take advantage of a 7-year adjustable rate and then refi in 2-3 years as rates return to normal. The main negative impact of higher rates is that they reduce the loan amount you qualify for.